Researched across Claude Opus, Grok Expert, Gemini Pro, and Perplexity Sonar. March 2026. Data sourced from Gartner, McKinsey, CB Insights, Menlo Ventures, Research and Markets, and Precedence Research.

The Gold Rush Nobody Told You About

In early 2025, a seven-person team of former YouTube engineers in Vienna quietly launched a SaaS tool that automatically converted long-form interviews into short-form clips optimised for TikTok, Instagram Reels, and YouTube Shorts. Within nine months, the product was generating $1.8 million in annualised recurring revenue with over 1,200 paying customers. No VC funding, no press tour, no unicorn mythology. Just a tightly focused, AI-native product slotted into a specific, painful workflow.

Welcome to the defining commercial pattern of 2026: the hyper-niche.

The era of growth-at-all-costs is over. The digital business landscape has undergone a ruthless but necessary correction. Founders and investors are no longer rewarded for building broad feature sets disguised as companies. The market now premiums indispensable, highly specific tools with solid unit-level profitability.

Here are the numbers that set the stage: Gartner estimates global AI spending will hit $2.52 trillion in 2026, up 44% year-on-year. Global SaaS end-user spending is projected to reach $375 to $465 billion this year alone, on a course toward $1.48 trillion by 2034.

What makes 2026 genuinely different is the convergence of three forces happening at the same time. First, AI inference costs have dropped over 90% since 2023. Second, infrastructure tooling like Supabase, Vercel, Cursor, and Replit lets a solo founder ship production-grade software in weeks. Third, entire industries including healthcare, legal, manufacturing, and logistics have barely begun their digital transformation. The question for founders in 2026 is not whether to start; it is exactly where to focus.

Key Takeaways at a Glance

Before we get into the full breakdown, here is a quick snapshot of what the research confirmed across four frontier AI models:

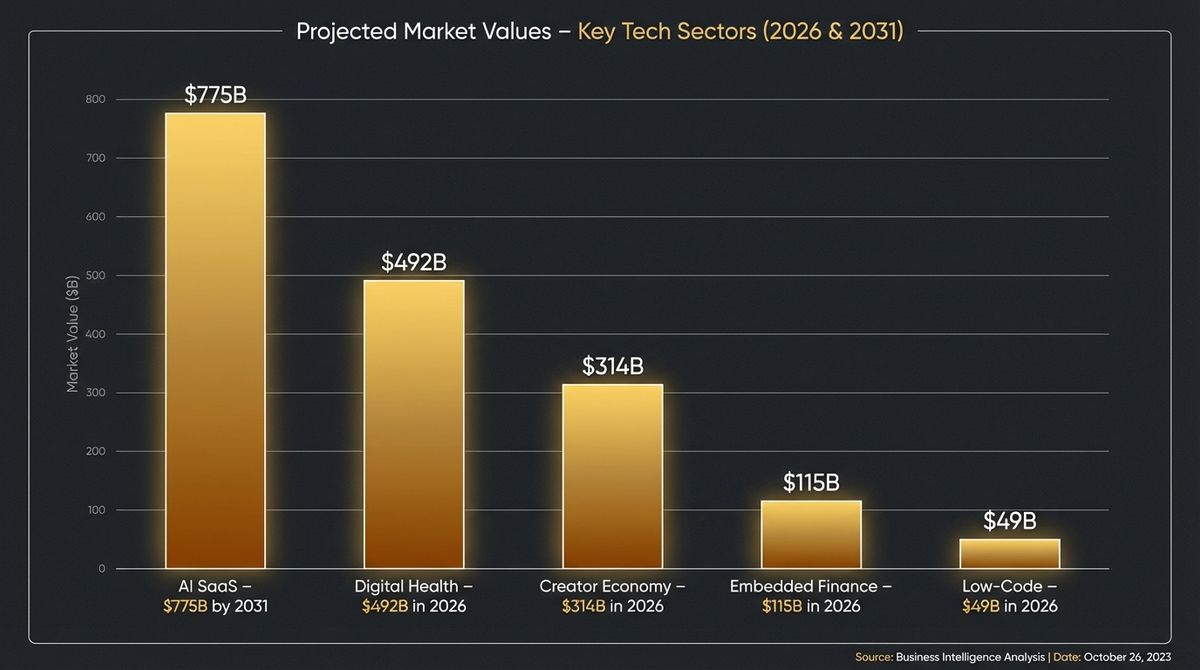

- AI-native products are the single fastest-growing digital business category, with AI SaaS growing at 38% CAGR, projected to reach $775 billion by 2031

- Vertical B2B SaaS offers the best risk-adjusted returns for most founders: high willingness-to-pay, low churn, bootstrappable from day one

- Creator economy infrastructure is a $314 billion market in 2026, growing at 23% CAGR toward $2 trillion by 2035

- Embedded fintech is where smart capital is flowing: the embedded finance market sits at $115 billion in 2026, growing to $250 billion by 2030

- Digital health is the highest-regulation but highest-moat category, with AI diagnostics companies capturing 54% of all health funding in 2025

- No-code/low-code platforms will power 75 to 80% of all new enterprise applications by end of 2026 (Gartner)

- The minimum viable skillset to launch in 2026: domain expertise plus one programming language or no-code platform plus distribution instinct

Market Context: Why 2026 Is the Real Inflection Point

By end of 2025, 95% of organisations had deployed AI-powered SaaS applications, and spending on AI-native apps surged 75% year-on-year (Zylo). OpenAI finalised a $110 billion funding round at a $730 billion valuation. Anthropic reached $14 billion in annualised revenue. Enterprise AI revenue tripled to $37 billion in 2025 (Menlo Ventures).

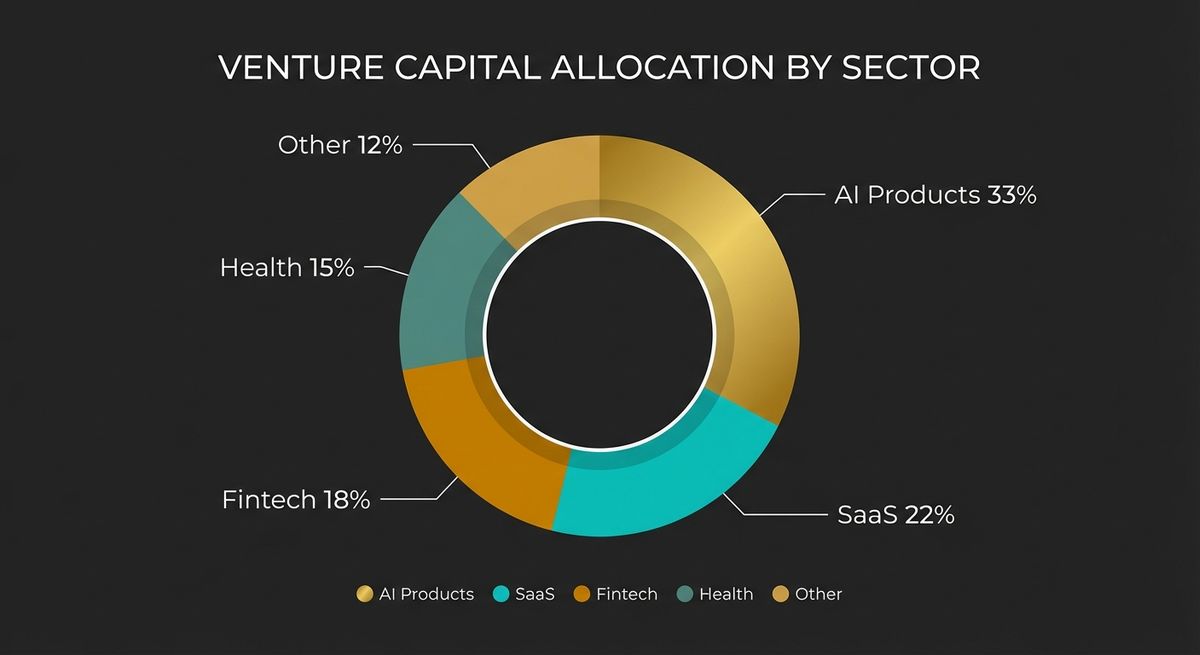

But here is what matters for builders: the application layer is finally getting serious attention. CB Insights reports that nearly two-thirds of new unicorns minted in 2025 had AI at their core. The concentration of GenAI funding in just a few foundation model companies is decreasing, which means vertical application startups are now attracting meaningful capital.

Gartner projects that by end of 2026, low-code platforms will account for 75% of all new application development. The low-code/no-code market itself is valued at $49 billion in 2026, projected to reach $239 billion by 2033. Tools like Cursor, Replit, Vercel, Supabase, and Bubble mean a single developer can now ship what used to require a team of ten at a cost of under $100/month in infrastructure. This compression of build cost is the single most underappreciated structural tailwind for first-time founders in 2026.

McKinsey's 2025 State of AI survey shows 72% of organisations now using AI in production, up from roughly 50% the year before. Agentic AI, where systems reason, plan, and execute multi-step workflows autonomously, is the defining technological paradigm of 2026 to 2028. The market for AI agents is projected to expand 33x from 2024 to 2028 (Gartner). Total global IT spending will hit $6.08 trillion in 2026, the first time it has crossed the $6 trillion threshold.

Three structural tailwinds are unique to this moment:

- Regulatory hardwiring: The EU AI Act and global data sovereignty laws have turned compliance-tech into mandatory infrastructure, creating entirely new startup categories

- Compute ubiquity: Localised, cost-effective AI compute is now a global commodity, enabling emerging markets like India to become world-class startup launchpads

- The solopreneur unicorn: AI-native development platforms now allow teams of 1 to 3 people to manage operations that previously required 50 or more employees

India specifically entered 2026 with 127 unicorns, 147 soonicorns, and over 2 lakh DPIIT-registered startups. This makes the analysis directly relevant for Indian-origin founders targeting global markets.

Top 10 Digital Business Categories for 2026

1. AI-Native Products and Vertical AI Agents

Market Size: Enterprise AI revenue reached $37 billion in 2025, tripling from the year before. The broader AI SaaS market grows at 38% CAGR, projected to reach $775 billion by 2031. In 2026, AI-focused startups attract approximately 33% of all global venture capital.

The Shift That Changes Everything

The critical distinction in 2026 is between "AI as a feature" bolted onto existing software and "AI as the entire product logic." The former is now table stakes, almost every SaaS product has an AI button somewhere. The latter, where the AI agent is the product, executing multi-step workflows autonomously without human hand-holding, is where the commercial opportunity lives. We are entering the age of "Outcome as a Service": buyers no longer pay for software seats, they pay for results delivered.

What does this mean practically? An AI legal agent is not a chatbot that answers questions about law. It is an autonomous system that reads a contract, identifies non-standard clauses, compares them against a client's risk tolerance, generates a redline, and files it, all without a junior associate touching it.

Specific Startup Ideas:

- AI agents for specific professional workflows: insurance claims processing, medical coding, IP filing, freight quote generation

- Autonomous SDR (Sales Development Representative) products that handle outbound prospecting end-to-end: research prospect, personalise email, send, follow up, qualify

- Domain-specific AI copilots for construction site safety auditing, agricultural yield planning, or logistics dispatch optimisation

- Voice-first productivity layers: ambient AI that takes push-to-talk notes and structures them into actionable meeting summaries (viable now because AI voice processing latency has dropped below the threshold of human perception)

- Agent marketplaces where users rent specialised agents for specific repeatable tasks: content repurposing, supplier onboarding, competitor monitoring

Why 2026 Is the Right Time: Agentic frameworks (LangGraph, AutoGen, CrewAI) have reached production stability. LLM inference costs have dropped to the point where bootstrapped founders can run AI-heavy products profitably. The "Agentic Summer" of 2025 proved these systems can handle real enterprise workflows. Now the application layer is being industrialised.

Required Skills/Resources: Prompt engineering, LLM API fluency (OpenAI, Anthropic, Google Gemini), ability to build reliable agent orchestration pipelines, and most importantly, deep domain expertise in your chosen vertical. Starting infrastructure budget: $500 to $5,000/month during development.

Revenue Potential: Vertical AI SaaS routinely charges $200 to $2,000/month per seat. Harvey (legal AI) reached an $8 billion valuation. Ambience Healthcare raised $243 million for clinical AI documentation. Even bootstrapped vertical AI tools in well-chosen niches can reach $10K to $50K MRR within 12 months.

Competitors to Study: Harvey (legal), Ambience Healthcare (clinical), Writer (enterprise content), Cursor (coding), Glean (enterprise search), Cognition AI's Devin (autonomous engineering).

⚠️ Risk Flag: Pure AI wrappers with no proprietary data or workflow integration are the least defensible products in 2026. The moat is not the model. Every founder has access to the same APIs. Build around proprietary data pipelines, workflow depth, and switching cost, not raw model capability.

2. SaaS Micro-Tools and Unbundled Software

Market Size: The global SaaS market is $375 to $465 billion in 2026, growing at 13 to 19% CAGR. There are over 30,800 SaaS companies worldwide. AI-enabled micro-SaaS is growing at approximately 38 to 40% annually relative to the broader market. Over 40% of new SaaS startups are deliberately targeting niche markets over mass audiences.

The Micro-SaaS Model

The defining insight of micro-SaaS: large platforms can never justify building features for every niche. A tool that serves 500 paying customers at $50/month ($300,000 ARR) is commercially meaningless to Salesforce. It is life-changing to a solo founder. And it is exactly what those 500 customers desperately need. There is something else working in micro-SaaS's favour in 2026: SaaS portfolio consolidation among enterprises has slowed dramatically, dropping from 14% to just 5% year-over-year (BetterCloud). Organisations are not cutting tools, they are replacing generic ones with specialised ones.

Specific Startup Ideas:

- AI-powered proposal generation tool specifically for freelance designers or creative consultants (not a generic document builder)

- Automated competitor monitoring dashboards for e-commerce brands with native Shopify integration

- Client portal builder designed exclusively for accountants or financial advisors (not every professional, just one)

- SOC 2 compliance automation for seed-stage startups ($5K to $50K/year market, underserved below Series A)

- Content repurposing pipelines: YouTube transcript extraction → AI restructuring → newsletter conversion, automated

- AI invoice dispute resolution for small businesses: reads invoices, flags discrepancies, drafts dispute letters

Revenue Potential: Micro-SaaS businesses commonly reach $5K to $50K MRR. Well-positioned tools can scale to $100K+ MRR. The economics are exceptional: low overhead, 80 to 90% gross margins, often fully bootstrappable. The exit market is active, with acquisitions of micro-SaaS tools generating $1M to $5M ARR common on marketplaces like Acquire.com and MicroAcquire.

Competitors to Study: Testimonial.to, Fathom Analytics, SavvyCal, Plausible Analytics, Bannerbear, TweetHunter.

3. Creator Economy Infrastructure

Market Size: The creator economy was valued at $254 billion in 2025 and is projected to reach $314 billion in 2026 (Precedence Research), growing at 23.4% CAGR toward $2 trillion by 2035. Goldman Sachs projects $480 billion by 2027. US influencer marketing spending alone hits $43.9 billion in 2026. Over 207 million creators are active worldwide.

The Infrastructure Gap

The creator economy has matured into a professional B2B sector, but the tooling has not kept pace. The opportunity is not to build another creator platform. It is to build the picks and shovels that creators use to run increasingly complex operations. Creators with three or more revenue streams earn $75,000 more per year on average than those relying on a single platform, according to creator economy research from 2025. They need accounting, CRM, analytics, licensing, and audience management, all built for the specific realities of their workflow, not adapted from enterprise software.

Specific Startup Ideas:

- Creator CRM: tracks brand partnerships, sponsorship deal pipelines, audience engagement, and revenue across YouTube, Instagram, TikTok, and Substack simultaneously

- AI persona licensing platform: allows creators to "rent" their digital voice or likeness for localised marketing campaigns while maintaining IP control and revenue share

- Cross-platform analytics dashboard: unified audience and revenue data across all channels in one view, with trend alerts

- Subscription/membership platform, specifically for educators and coaches. Not a generic platform, but one with built-in cohort scheduling, assignment delivery, and completion tracking

- Micro-influencer management dashboard with built-in affiliate automation, payment processing, and performance attribution for brands working with 50 to 500 nano-influencers simultaneously

Why 2026 Is the Right Time: 84% of creators already use AI tools. Micro and nano-influencers will claim 45.5% of all influencer marketing spend in 2026 (eMarketer), meaning the market is broadening far beyond top-tier talent. Creators are aggressively diversifying away from ad-revenue dependency toward direct-to-fan monetisation, digital products, and IP licensing, creating entirely new tool categories that did not exist three years ago.

Revenue Potential: Creator tools price at $15 to $100/month for individuals, $200 to $1,000/month for agencies and brand teams. Platforms handling transactions charge 10 to 20% commissions. Kajabi reached $100 million ARR serving the creator-educator market. Substack's model demonstrates billion-dollar platform scalability.

4. No-Code and Low-Code Application Builders

Market Size: The low-code development platform market is valued at $49 billion in 2026, projected to reach $239 to $377 billion by 2033 to 2034 at 25 to 29% CAGR (Persistence Market Research / Fortune Business Insights). Gartner projects 75% of all new enterprise applications will use low-code/no-code technology by end of 2026.

The Citizen Developer Economy

There is a global shortage of software developers. This gap drives powerful, structural demand for tools that let non-developers build functional, production-grade software. The fastest-growing vertical for low-code adoption is healthcare at 29% CAGR, followed by financial services and manufacturing. India specifically saw a 45% increase in enterprise low-code deployments in 2025, making it one of the most active markets globally for this category.

The interesting insight here: the opportunity is not to build yet another generic no-code platform that competes with Bubble or Webflow. The opportunity is to build vertically specialised no-code builders or template ecosystems that serve a very specific industry with pre-built logic, compliance frameworks, and integrations baked in.

Specific Startup Ideas:

- Industry-specific no-code builders: real estate agent client portals, restaurant management dashboards, HVAC service dispatch systems

- Middleware template libraries connecting legacy ERPs and databases to modern no-code frontends

- Enterprise Agent Studio: a drag-and-drop interface for compliance officers and fraud analysts to build their own investigative AI workflows without writing code

- No-code mobile app builder with native AI features embedded (voice commands, document scanning, intelligent autofill)

- Template marketplaces for Bubble, Glide, and FlutterFlow ecosystems: curated, industry-specific, premium

- Workflow automation tools specifically for Indian MSMEs with vernacular language support, GST integration, and UPI-native payments

Revenue Potential: Platform subscriptions range from $25/month (prosumers) to $5,000/month (enterprises). Marketplace models generate additional revenue through template sales and rev-share. Well-executed vertical no-code tools commonly reach $50,000 MRR within 18 months.

Competitors to Study: Bubble, Retool, Make.com, WeWeb, FlutterFlow, Glide, Airtable, Softr.

5. Digital Health Products

Market Size: The digital health market is estimated at $380 to $492 billion in 2026 (Fortune Business Insights), growing to $2.35 trillion by 2034 at 19 to 22% CAGR. Digital health funding reached $14.2 billion in 2025, with AI-focused companies capturing 54% of all health investment.

Regulation as Moat

Digital health is simultaneously the highest-barrier and highest-moat category in this list. The regulatory burden (HIPAA, GDPR, India's DPDP Act, FDA clearance) is enormous. But that is precisely the point. Once your product is compliant and integrated into clinical workflows, switching costs are prohibitive. The barriers that seem daunting upfront become your greatest competitive protection once cleared.

Oura generated $1 billion in revenue in 2025 and projected doubling in 2026. The FDA's January 2026 reclassification of non-invasive monitoring devices opened new product categories, particularly in continuous glucose monitoring and AI-driven chronic disease management. In India, the ABDM (Ayushman Bharat Digital Mission) has created a health data interoperability layer that makes API-native health startups far more viable than they were two years ago.

Specific Startup Ideas:

- Bio-digital twin dashboards: integrates Oura/Apple Watch/CGM data with bloodwork APIs (Vital.dev, Quest Diagnostics) for real-time biological age tracking and personalised health intervention recommendations

- AI symptom triage chatbot for specific chronic conditions. Not a general health chatbot, but one trained deeply on, say, diabetes management for South Asian patients (a grossly underserved market)

- Wearable data aggregation platform converting multi-device health data into actionable clinical insights, sold B2B to corporate wellness programs

- Remote patient monitoring for Tier 2 and Tier 3 Indian cities, where telehealth infrastructure is newly built but digital health tooling is minimal

- AI-powered prior authorisation automation for healthcare providers that reduces administrative burden by 70%+, with a clear, provable ROI

Revenue Potential: B2B digital health products command $500 to $10,000/month per clinic or hospital. B2C health apps charge $10 to $50/month, with premium tiers. B2B2C through corporate wellness programs can generate $1M+ ARR with under 100 enterprise clients.

Key Risk: Start in regulatory-permissive use cases first (wellness, not diagnostic). Build compliance infrastructure early; retrofitting HIPAA compliance is significantly more expensive than designing for it from the start.

6. Fintech Infrastructure and Embedded Finance

Market Size: The embedded finance market sits at approximately $115 billion in 2026growing to $250 billion by 2030 at 21.5% CAGR (Research and Markets). The Asia-Pacific region is the fastest-growing area, bolstered by mobile-centric digital ecosystems. India's UPI infrastructure gives Indian-origin startups a 3 to 5 year structural head start on much of the Western world.

Infrastructure, Not Consumer Apps

Consumer fintech is crowded and brutally regulated. The real opportunity in 2026 is one level deeper: the infrastructure that powers other businesses' financial features. Think Banking-as-a-Service, embedded lending, white-label payment orchestration, and the "platformisation" of B2B commerce, where non-financial vertical SaaS platforms embed accounts, lending, and insurance directly into their ERP workflows to monetise their existing user base.

This "platformisation" trend is the single most important dynamic in fintech today. A logistics SaaS platform that manages 5,000 trucking companies can embed invoice factoring into their product, charging a 2 to 3% fee on every advance, without becoming a bank. The SaaS platform wins (higher ARPU, stickier product). The trucker wins (faster cash). The embedded finance provider wins (volume at scale). Everyone wins except the legacy bank getting disintermediated.

Specific Startup Ideas:

- Embedded lending API for vertical SaaS platforms serving SMBs. Plug-and-play revenue-based financing that the SaaS platform can offer under their own brand

- Compliance automation SaaS for fintechs navigating multiple regulatory jurisdictions (India's RBI, EU's PSD3, US's evolving rules)

- Cross-border B2B payment infrastructure for Indian exporters/importers dealing with the fragmentation of SWIFT, SEPA, and UPI

- Real-time treasury management tools for Indian MSMEs that automate reconciliation, tax provisioning, and cash flow forecasting

- AI-powered fraud detection-as-a-service for payment processors and neo-banks in Southeast Asia

- KYC/AML automation APIs specifically built for emerging-market regulatory requirements

Required Skills: API design, financial regulation literacy, and critically, the ability to build trust with enterprise clients. Fintech sales cycles are long (6 to 18 months), so runway and patience are requirements.

Revenue Potential: Fintech infrastructure businesses typically charge per API call, per transaction (0.1 to 0.5%), or via SaaS tiers ($500 to $50,000/month for enterprise). Stripe's valuation demonstrates the ceiling of this model. Even at much smaller scale, B2B fintech infrastructure businesses generating $500K ARR are highly acquirable.

Competitors to Study: Stripe, Razorpay, Setu (India), Unit, Bond, Synctera.

7. EdTech 2.0: Outcomes-Driven Learning

Market Size: The global e-learning market is valued at over $400 billion in 2026. Corporate e-learning sits at $50 billion. The K-12 EdTech market is $25 billion. AI tutoring applications are growing at 34% CAGR.

The Credentialling Crisis

Traditional degrees are losing their monopoly on signalling professional competence. Employers, particularly in tech, finance, and consulting, are moving toward skills-based hiring. This creates a massive opportunity for platforms that offer verifiable, outcome-linked credentials rather than certificates of attendance. The edtech failures of the 2021 to 2023 cohort (Byju's, Unacademy's struggles) were almost uniformly failures of outcomesnot technology. The 2026 opportunity is specifically about building learning products where the revenue model is directly tied to learner outcomes: income sharing, job placement fees, employer licensing.

Specific Startup Ideas:

- AI tutor for niche professional certifications: not a broad learning platform, but an AI that can take a learner from zero to passing a specific exam (CFA Level 1, NISM Series VIII, AWS Solutions Architect) in 8 weeks

- Corporate training platform with AI content generation: personalised employee training with adaptive learning paths, sold directly to HR/L&D departments at $15 to $40 per employee per month

- Cohort-based learning platform for expert instructors who want to run live courses with community features, charging 10 to 20% of course revenue instead of a flat subscription

- Micro-credential marketplace for practical skills with employer verification (think: LinkedIn Learning but with actual skill assessments that companies trust)

- AI-powered language learning for professional contexts. Not Duolingo-style gamification, but business English, interview preparation, or legal Hindi for specific career tracks

Why 2026 Is the Right Time: Companies spend an average of $1,300 per employee annually on training. Cohort-based courses show 10x higher completion rates than self-paced alternatives. AI now makes personalised 1:1 tutoring economically viable at scale. Khanmigo proved the model, and the application layer is wide open.

Revenue Potential: B2C learning tools price at $30 to $100/month. B2B corporate training at $15 to $40/employee/month. A platform serving 10 mid-sized companies of 200 employees each at $25/month generates $600K ARR, fully bootstrappable.

Competitors to Study: Khanmigo (Khan Academy AI), Maven, Coursera for Business, Learnworlds, Teachable, Internshala (India).

8. E-Commerce Infrastructure and DTC Tooling

Market Size: Global e-commerce is projected at $6.9 trillion in 2026. Shopify alone powers over 10% of US e-commerce. The real opportunity is not running a store. It is building the infrastructure, tooling, and services that the 26 million+ e-commerce merchants worldwide rely on.

The Picks and Shovels Play

Every time a gold rush happens, the people who reliably profit are the ones selling picks and shovels. The same logic applies to e-commerce. Building a DTC brand is brutally hard in 2026. Customer acquisition costs have tripled since 2020, and brand building takes years. But building tools for the millions of merchants already in the game? That is a B2B SaaS play with a defined buyer, a clear pain point, and a measurable ROI.

Specific Startup Ideas:

- AI-powered product listing optimisation that automatically rewrites product descriptions for SEO, A+ content, and regional language variants, sold as a Shopify app or standalone API

- Post-purchase retention automation: AI sequences that personalise post-purchase emails, SMS, and WhatsApp touchpoints based on product category, customer lifetime value, and churn signals

- Supplier discovery and verification platform for Indian exporters and D2C brands sourcing from tier-2/tier-3 manufacturing clusters

- Returns management and reverse logistics SaaS specifically for Indian e-commerce, an Rs. 89,000 crore problem with no dominant solution

- Headless commerce component library: pre-built, performant storefront components for developers building on Next.js + Shopify Hydrogen or Medusa.js

- AI-driven demand forecasting and inventory management for small Shopify merchants (sub-$1M GMV), underserved by enterprise tools like NetSuite

Revenue Potential: Shopify app stores generate apps that earn $10K to $500K+ MRR. Service-oriented infrastructure businesses command monthly retainers or per-transaction fees. The acquisition market is active: Shopify-ecosystem companies with $500K+ ARR regularly command 4 to 6x revenue multiples.

Competitors to Study: Klaviyo, Gorgias, Recharge, Loop Returns, Skio, Postscript.

9. API-First Businesses and Developer Tools

Market Size: The global API management market is valued at approximately $8 to $10 billion in 2026, growing to $30+ billion by 2030 at 28%+ CAGR. Developer tool spending grew 35% year-on-year in 2025. Over 90% of new software applications now rely on external APIs.

Why Developers Are the Best Customers

Developers are, arguably, the best B2B buyers in the world. They self-educate, they self-serve, they do not need a sales rep, and when they find a tool they love, they embed it so deeply into their infrastructure that switching is practically impossible. The most valuable developer tool companies (Stripe, Twilio, Segment, Cloudflare) all shared the same growth pattern: start with a clean, beautiful API, build extraordinary documentation, give developers immediate value, and charge based on usage as they scale.

Specific Startup Ideas:

- Compliance data APIs: expose regulatory datasets (RBI circulars, SEBI filings, MCA records) as clean, structured JSON APIs that developers can query programmatically

- AI observability and evaluation tooling that helps teams monitor LLM performance, detect hallucinations, and evaluate prompt changes at scale. Think "Datadog for AI applications"

- Webhook reliability infrastructure with guaranteed delivery, retry logic, and event replay for SaaS products. A small but genuinely painful problem that every developer faces

- Data enrichment APIs for India-specific B2B contexts: company information, GST data, director details, credit signals, all verified and structured

- Notification orchestration API: a single API for email, SMS, WhatsApp, and push notifications, with intelligent routing based on user engagement patterns

- Identity verification and KYC APIs with native India stack integration (Aadhaar, DigiLocker, PAN), sold to fintechs, lending platforms, and crypto exchanges

Revenue Potential: Usage-based API businesses generate revenue that scales with customer growth, not just seat count. At $0.001 to $0.01 per API call, a product making 10 million calls per day generates $30K to $300K MRR. The compounding revenue dynamic, combined with very low churn, makes API businesses extremely attractive to acquirers and investors.

Competitors to Study: Stripe (payments API), Twilio (communications), Setu (India data APIs), Sendbird (chat API), Apideck, Courier.so.

10. Niche B2B Software for Underdigitised Verticals

Market Size: B2B software for underdigitised industries is an enormous, fragmented, and largely undercounted market. Construction alone is a $13 trillion industry globally with software penetration under 20%. Agriculture ($3.5 trillion global), logistics, legal, insurance, and manufacturing share similar profiles: enormous revenues, low software adoption, and incumbents using software that was built in the 2000s.

The Last White Space

Consumer software is fully digitised. Enterprise software is deeply contested. The genuine last frontier is the massive middle of the economy: mid-market companies in "boring" industries that are under-served by both consumer apps (too simple) and SAP (too expensive). A plumbing company with 40 technicians generating $8M/year does not need Salesforce. It needs scheduling, invoicing, inventory, and customer communication in one product built specifically for their workflow.

Specific Startup Ideas:

- Legal operations SaaS for Indian law firms: matter management, document drafting with AI, billing, and client portal. An industry still heavily reliant on WhatsApp and paper

- Construction site management platform: daily progress reports, worker attendance, material tracking, and subcontractor management with WhatsApp-native input (because construction workers do not use desktop software)

- Agri-supply chain platform connecting farmers in UP/Bihar directly to FMCG procurement teams, with quality grading, payment processing, and logistics embedded

- Staffing agency management software for contract workforce deployment: tracking placements, compliance, and payroll for labour contractors in manufacturing zones

- Insurance claims workflow automation for GI (General Insurance) companies in India. An industry where 60% of processes are still manual and fraud detection is reactive

Why 2026 Is the Right Time: The GST network, UPI, and ONDC have created a digital spine for Indian commerce. MSME digitisation is being actively incentivised by government policy. The founders best positioned to capture these opportunities are those with domain expertise from within these industries, not outsiders guessing at pain points.

Revenue Potential: Vertical SaaS for SMBs charges $50 to $500/month. For mid-market clients ($10M to $100M revenue), contracts of $2,000 to $20,000/month are standard. A portfolio of 100 mid-market construction clients at $1,000/month is a $1.2M ARR business achievable in 24 to 36 months.

Competitors to Study: Procore (construction), Veeva (pharma), Toast (restaurants), AgriStack (India), Farmlink.

How to Evaluate a Digital Business Opportunity in 2026

Not all market opportunities are equal. Before committing to an idea, run it through this four-dimension framework:

1. Pain Intensity (the "painkiller vs. vitamin" test)

Is the customer losing money, time, or compliance standing without your product? Painkillers command premium pricing and generate urgency. Vitamins get deprioritised in budget cuts.

2. Willingness to Pay (the checkout test)

Can you get someone to give you a credit card number before you build the product? This is the most reliable signal of real demand. A waiting list with emails is encouraging. A waiting list with $99 pre-payments is confirmatory.

3. Distribution Advantage (the "how do you get the first 100 customers" test)

Every category described above has a clear distribution path. If you cannot articulate how you would get the first 100 customers specifically (not "content marketing" or "social media" but the exact channel and motion), the idea is not yet ready to build.

4. Defensibility Horizon (the "what happens in year 3?" test)

AI wrappers commoditise in 12 to 18 months. Proprietary data, deep workflow integration, network effects, and regulatory compliance do not. Before you start, map out what makes your business harder to copy in year 3 than in year 1.

High-Confidence Findings (All Models Agreed):

- AI-native, vertical-specific SaaS is the single best digital business category for 2026 (all four models ranked it first or second)

- Creator economy infrastructure is significantly larger than most founders realise; the infrastructure gap is unanimously identified as more valuable than building new creator platforms

- The embedded finance opportunity is real, structural, and underpenetrated, particularly in Asia-Pacific

- Low-code/no-code is a sustained, decade-long tailwind, not a hype cycle. The enterprise adoption data is unambiguous

Points of Disagreement:

- EdTech's recovery: Grok and Gemini were bullish on EdTech's recovery in 2026, pointing to AI tutoring adoption and cohort-based learning growth. Claude and Perplexity were more cautious, noting that Byju's collapse and over-funding of 2021-era edtech has created lasting investor scepticism in the category. Reconciliation: EdTech is a strong opportunity for bootstrapped or lightly funded founders building specific, outcome-linked products. It is a difficult fundraising story for VC-backed companies in the near term.

- Consumer vs. B2B fintech: Models diverged on whether consumer-facing fintech still has a viable opening. Reconciliation: Consumer fintech built on top of infrastructure (super-apps, embedded wallets) is viable. Standalone consumer fintech apps competing with BHIM/PhonePe/GPay on commoditised features are not.

- Web3 and tokenised economies: Grok included tokenised creator economies and RWA (Real World Asset) tokenisation as significant 2026 opportunities. Other models were sceptical. Reconciliation: Meaningful but early-stage; risk-tolerant founders with regulatory patience may find genuine opportunity in RWA tokenisation, particularly for real estate and private credit.

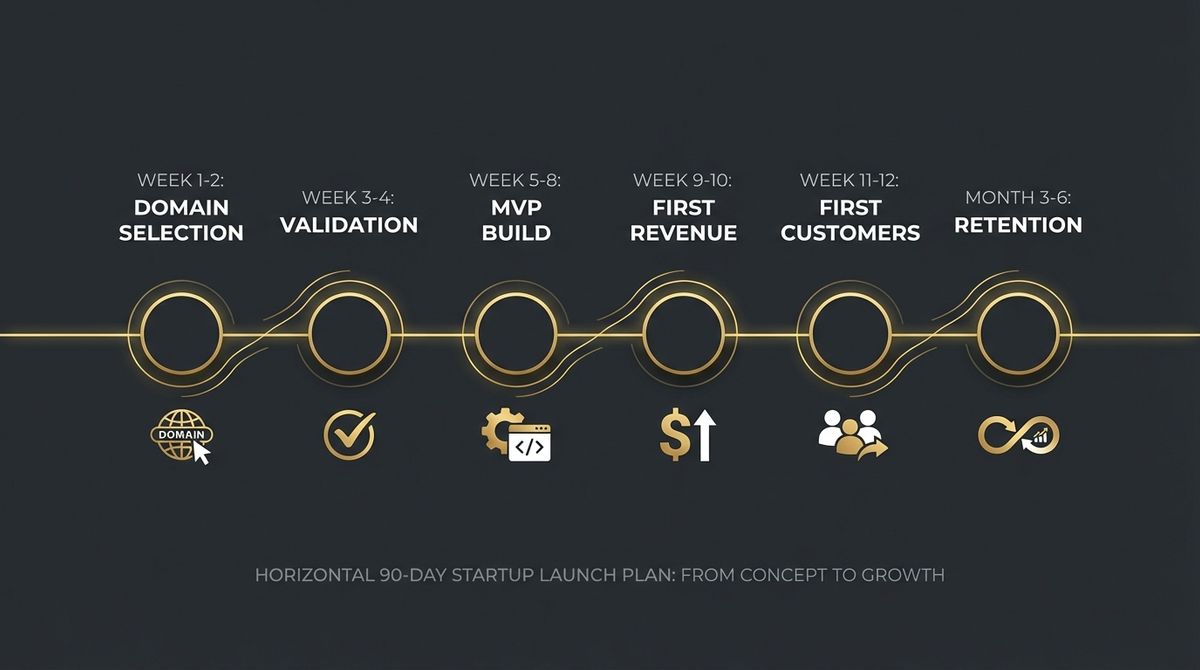

Actionable Steps: From Idea to First Revenue in 90 Days

- Week 1 to 2: Domain Selection Choose the industry you will serve based on your existing knowledge and access, not based on market size alone. The biggest competitive advantage a founder has is domain expertise that outsiders cannot replicate quickly.

- Week 3 to 4: Problem Validation Have 15 unscripted conversations with potential customers. Do not pitch your product. Ask: "Walk me through the most painful part of your week." If the same workflow appears across 10+ conversations, you have found a real problem.

- Week 5 to 8: Painfully Narrow MVP Build the minimum product that directly addresses the single most painful part of that workflow. Not a feature-complete platform. A focused, opinionated tool that does one thing better than anything else available. Use Cursor, Supabase, and Vercel to ship fast.

- Week 9 to 10: Charge From Day One The single most common mistake of first-time founders is building for too long without charging. Set a price before you build. Get a credit card number before you write the first line of code if at all possible.

- Week 11 to 12: First 10 Customers Distribution is the job now. The channels that work for niche B2B products in 2026: direct outreach on LinkedIn, posting in niche communities (Reddit, Discord, Slack groups, WhatsApp groups for your industry), and content that demonstrates domain expertise, not product demos.

- Month 3 to 6: Iterate on Retention First, Growth Second A product that 10 customers love and use every week is a stronger foundation than a product that 100 customers tried once. Build for retention before you optimise for acquisition. The SaaS metrics that matter at this stage: weekly active usage and churn, not MRR.

Conclusion: The Most Important Thing

The digital business landscape in 2026 is simultaneously the most competitive and the most accessible it has ever been. The tools available to a solo founder today (AI coding assistants, cloud infrastructure at commodity prices, global payment rails, and distribution platforms that reach billions of people) would have required a $10 million seed round to assemble just six years ago.

But abundance of tools has not made success automatic. If anything, the proliferation of cheap software has raised the bar for what counts as genuinely valuable. The businesses that win in 2026 will not win because they used AI. Every competitor will. They will win because they understood a specific human problem better than anyone else, built something indispensable around it, and found the customers who needed it most.

The gold rush is real. The picks and shovels are cheap. The question is whether you know the terrain well enough to dig in the right place.

Frequently Asked Questions

Q: What is the best digital business to start in 2026 with no funding?

Micro-SaaS, niche B2B software, or creator economy tools. All three can reach $10K to $50K MRR bootstrapped. The pattern: find a specific, painful, repeatable workflow in an industry you know, charge $50 to $500/month, and focus on distribution before features.

Q: Is it too late to build an AI product?

No. The application layer of AI is in its early innings. Most professional verticals (law, construction, agriculture, healthcare, education) remain almost entirely untouched by AI-native tooling. The question is not whether to build AI into your product; in 2026 that is a given. The question is which specific workflow you are going to automate better than anyone else.

Q: How much money do I need to start a digital product in 2026?

A solo founder with technical skills can launch a functional SaaS product for under $500/month in infrastructure. The real investment is time. Three months of focused evenings and weekends can produce a product that is genuinely ready for paying customers. AI coding tools (Cursor, Claude Code, GitHub Copilot) have reduced the time-to-MVP by 60 to 70% since 2023.

Q: Which digital business categories are best for India in 2026?

India-specific highest-conviction bets: B2B fintech infrastructure (leveraging UPI/Aadhaar stack), niche B2B software for MSMEs in manufacturing/construction/logistics, digital health for chronic disease management in tier-2/3 cities, and EdTech for professional certification and skill credentialling. India enters 2026 with the infrastructure, the talent, and the market scale to build globally relevant companies from day one.

Q: What is the realistic timeline to profitability for a digital product startup?

For a bootstrapped SaaS or API-first product targeting B2B, the realistic timeline to break-even (covering a founder's market-rate salary equivalent) is 12 to 24 months for a focused execution. For VC-backed startups optimising for growth, profitability timelines extend to 36 to 60 months. The 2026 market rewards capital efficiency significantly more than 2021 did.

Q: How important is SEO and content marketing in 2026?

Critical, but the strategy has shifted. Traditional keyword-ranking SEO remains valuable, but AEO (AI Answer Engine Optimisation) is increasingly important as more search traffic routes through AI-powered engines (ChatGPT, Perplexity, Google AI Overviews). Structure your content to answer specific questions directly, use clear headings, include data and citations, and build topical authority over a defined subject area.